Assisted over 100,000 small Indian businesses access loans.

Small business is the backbone of the Indian economy. Families take care of themselves by operating their own small scale manufacturing businesses or small retail shops. These small businesses are ubiquitous across India and are run in a similar manner from family-to-family.

Before Vistaar Financial Services started offering small business loans, many business owners couldn’t get credit from banks because they didn’t have the documents that banks required such as tax returns and bank accounts. Also, the process was difficult to navigate for most small business owners, making it difficult to qualify.

This limited the potential of small businesses because they couldn’t obtain loans to expand, or if they wanted a loan, they were forced to take high interest loans from local money lenders.

As Vistaar’s Lead Product Manager, my main responsibility was conducting extensive research on small businesses. Our research would lead to insights into how these businesses ticked to figure out how might we build tools to assist the branch staff with the lending decision without putting a burden on our clients.

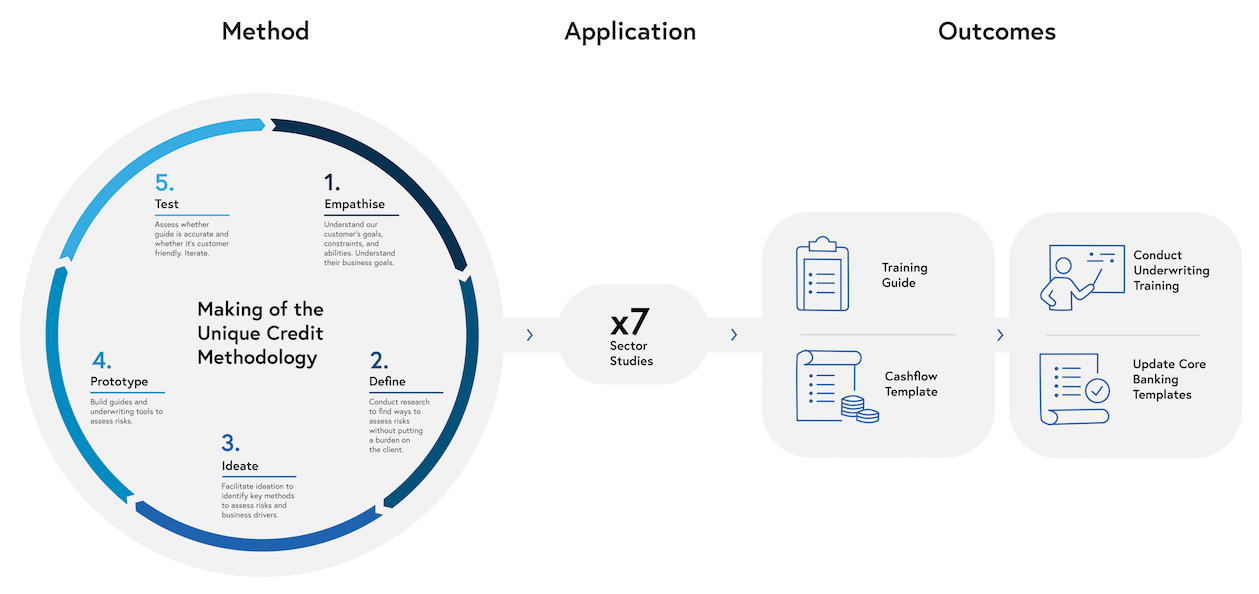

This Unique Credit Methodology was underpinning the Vistaar’s customer value proposition and its ability to scale. These tools have helped small businesses assess over 100,000 loans and enabled the firm to expand from 25 branches to over 200 branches today.

Image from Vistaar

Who Was Involved

I conducted this work under the Head of Risk (Sankar Sastri), and I led a small team of people that assisted with the interviews and data collection. The staff at each individual brach was vital in making this work possible. They scheduled the interviews with the business owners, organised logistics, and often worked as my hosts, emergency translators, and overall problem solvers.

My Role

In 2012 the world of international social impact business opened its doors to me when I started working for Vistaar Financial Services in Bangalore, India. In the first week I stepped into the Vistaar office, the Head of Product passed his work load to me so that he could focus on other responsibilities. Financial product design work had been put on my desk. I didn’t seek it out, but I loved it.

Although credit underwriting isn’t normally thought of as a financial product, at Vistaar it was a differentiating service as it allowed the firm to assess clients that traditionally were not able to obtain bank loans. The branch level member of the risk team would go to the clients business, ask a series of question, observe, use non traditional documents to estimate their income, and then verify their income using investigative inquiry. The tools I made would make this process possible.

What we did

During the two years that I worked with Vistaar, I conducted research across 7 sectors. Each piece of research usually took 6-8 weeks with half of that time spent travelling and interviewing. It was important to conduct research across multiple locations so that research wouldn’t be biased towards a particular location. I conducted more than 200 onsite interview over 2 years.

The objective of this research was to produce two artifacts: a sector specific training guide to help the risk team accurately assess businesses in this sector and a cashflow template to help estimate business and personal expenses with limited information. The cashflow template was then be built into the core banking system.

There were two main types of work: updating an old underwriting template and creating new underwriting for a previously not researched sector. Each piece of work was similar as we understood the How Might We. For a particular sector, How Might We best build tools to assist branch staff with the lending decision without putting an unrealistic burden on our clients.

We were taking a process that is done throughout the world (the decision to lend money or not to lend money) and adjusting this practice to the local conditions of India and specifically to a particular industry in India.

We started with learning about our customers and their businesses. I collected information from stakeholder interviews and secondary research to learn as much as possible about the industry, although there was usually very little applicable secondary research on micro and small businesses.

The research interviews usually started in an unstructured exploratory style to get to know the customer and became more structured as we found insights and validated these insights. There was also a qualitative part of our interviews so that we could understand business margins and prospective internal rate of returns for business investments.

The new underwriting training guide and cashflow template was tested for accuracy prior to launch. We updated the artifacts based on what we learned from the tests. Once launched, we conducted a training with each branch level risk team and incorporate the templates into the banking system to simplify data entry.

What we learned

This was a trial by fire for my interview abilities. By researching, reading, and doing, I learned the core of interviewing. I learned to plan, build guides, iterate. I learned what I have come to believe are the most critical aspects of interviewing - curiosity and empathy.

Conducting interviews across cultures and in using multiple languages is challenging. I learned how to navigate interviews across different languages. How to work with translators and to ask questions in multiple ways to triangulate on pieces of information and to avoid insights being lost in translation. Interviewing through a translator is never ideal, but with a well organised interview guide that have been tested and iterated, these challenges can be overcome.

This research taught me about business. When I worked in finance earlier in my career, I looked at large businesses as complex entities because I was trying to understand them through their financial statements. At the time, I didn’t actually understand what business was. This research taught me that businesses per se aren’t complicated; people are what make business complicated and interesting.

Small things can transform peoples lives. If a family that currently operates one power loom receives a loan and invests it in another power loom, they can almost double their income, improving their lives and the lives of their children.